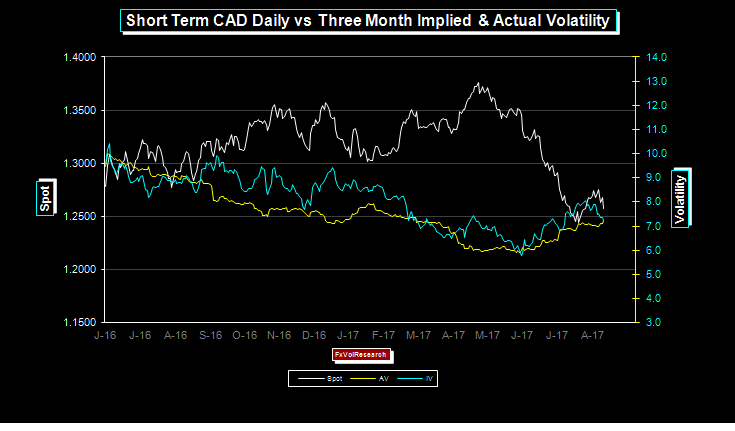

Three month CAD implied vols moved lower on the week as the spot consolidates. IV-AV spreads are back to flat. The move also takes out the rising trend line in the implied vol trend.

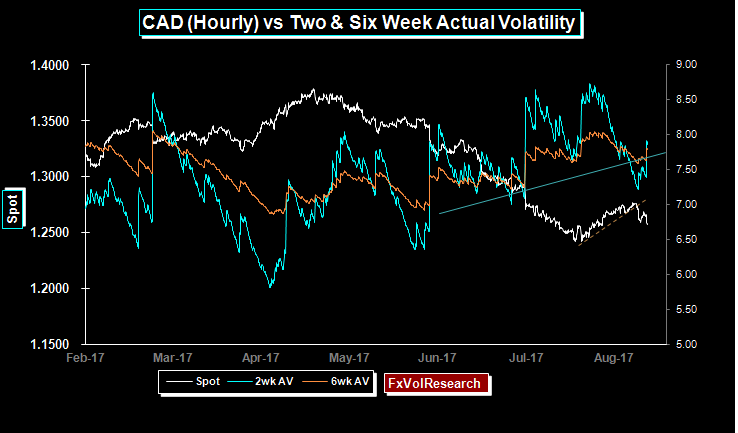

However, while longer dated vols fell actual vol in the short term rose and two week AV ended above 6 week AV. The spot has not yet settled down and short dated C$ options are oversold (see below).

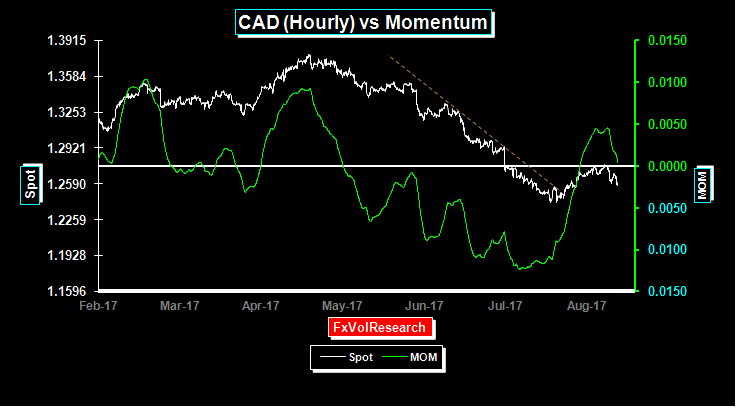

Fridays correction has brought momentum back to flat.

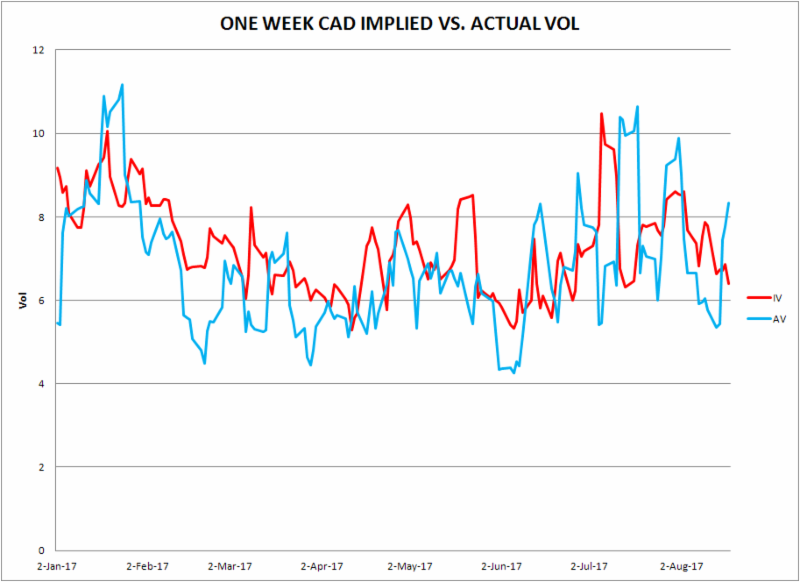

Notice the divergence between one week implied and actuals. One week CDN implied ended lower while actuals rose. The short dates have been sold off too far too fast. Look at data from the start of the year, getting long the one week around the 6% level has proven a good bet on higher actual vol.

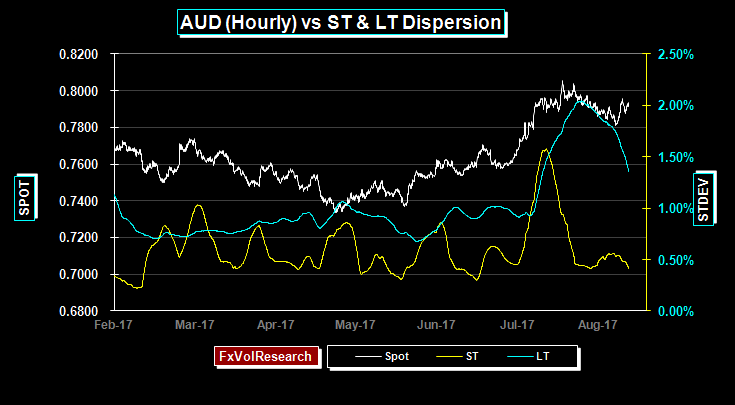

AUD momentum is back to flat, while the LT and ST dispersion readings are still declining. This increases the odds of price consolidation in the near term. A longer term directional trend in the AUD is unlikely to be developing soon.

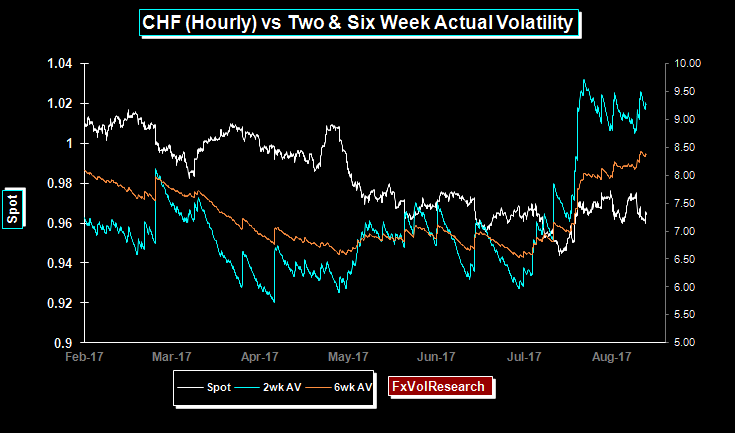

Short term CHF actual vols remain elevated. This pattern is often observed ahead of a longer term rising volatility enviornment.

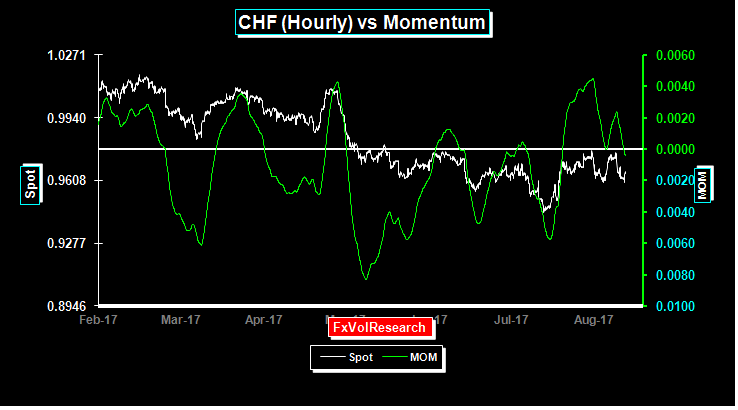

CHF momentum turns negative.

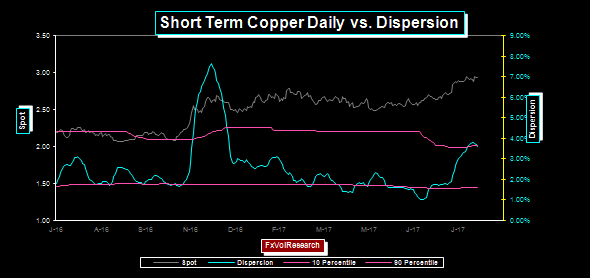

Copper remains a good proxy for the trend in the global economy. Synchronized global growth implies better copper demand, particularly from China. Copper has been rising but with declining volatility and now may be showing some signs of consolidation as it approaches the 3.00 level. A break higher above 3$ would take out a lot of top side resistance and suggest a further acceleration of global growth. The chart above with dispersion declining implies a period of short term consolidation in the near term. By implication global growth may start to level off.

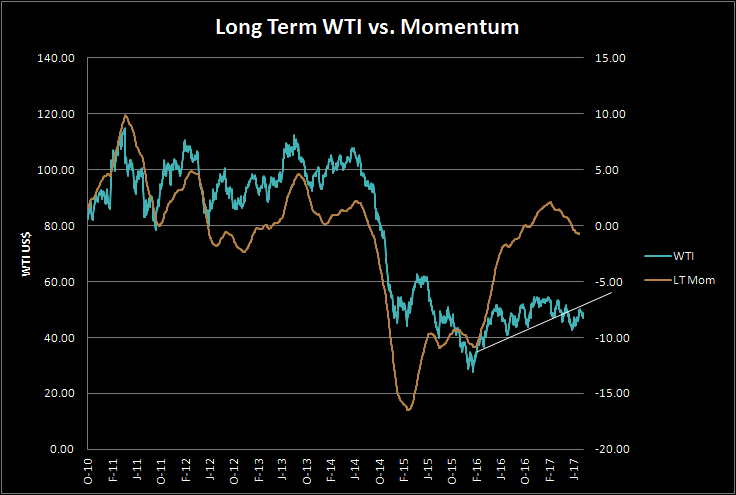

WTI had a 3% plus daily move higher on Friday, however, if you look at the long-term chart vs. momentum, WTI has significant topside resistance. At the same time, we are still below the short term trend line in the chart above.

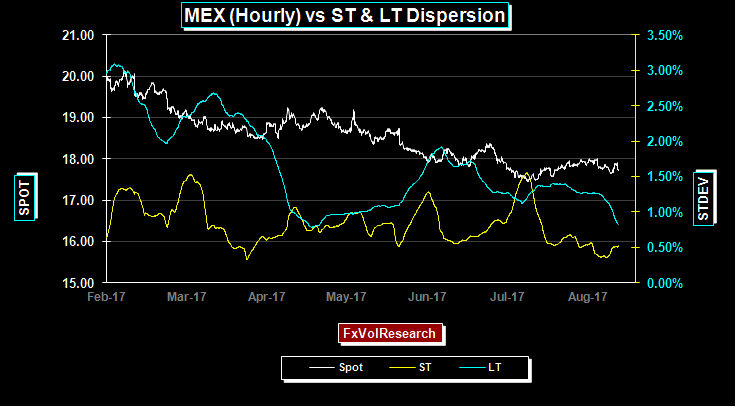

Based on our own percentile readings MXP vols are getting cheap, however, the very powerful downtrend in MXP implied volatility remains very much intact. MXP risk reversals have also declined from their recent highs in favor of the Dollar. The gap between 3M and 12M MXP risk reversals has narrowed. With LT dispersion still falling implied vols can still trend lower still.

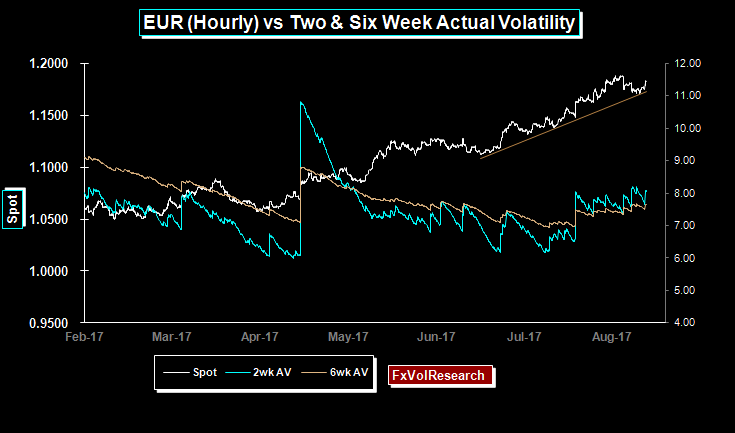

Like the CHF, the EUR actuals are starting to trend higher. The choppy price action has not violated the longer term uptrend.

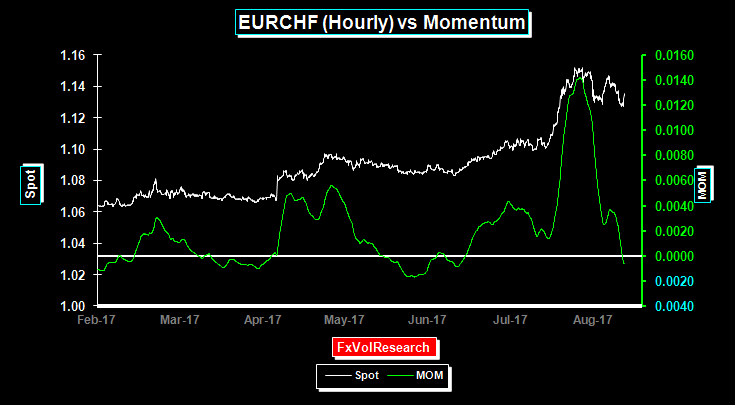

With the choppy price action, EURCHF has lost its topside momentum.

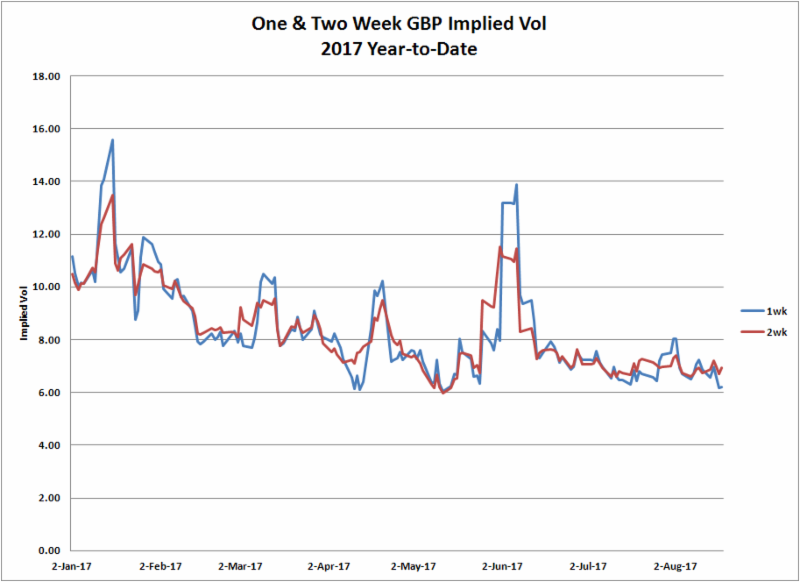

The market tends to sell off short dated vols ahead of holidays. The upcoming UK holiday on the 28th is no exception. In this case, it has sold the one week off too far. One week GBP at 6% is out of line with the actuals. Despite the upcoming bank holiday week end the premiums are too cheap.

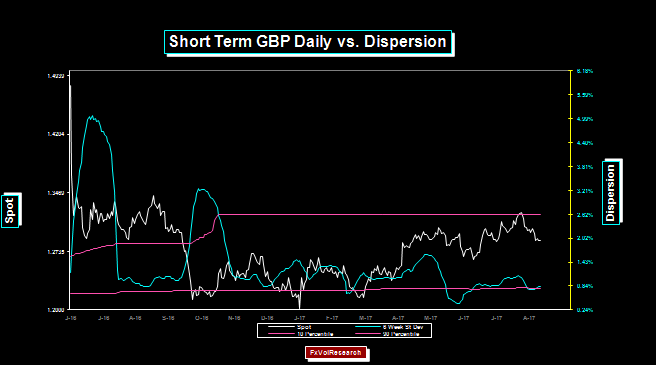

Low dispersion reading suggests a higher probability of short-term trend developing in GBP. This is another reason not to short the short dated options but rather to be long.

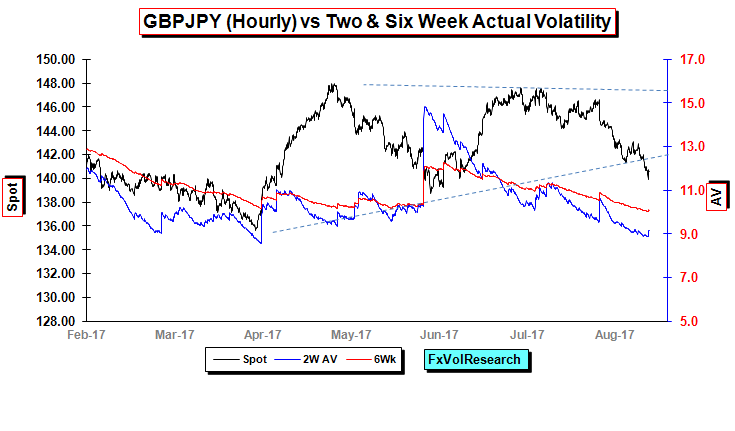

GBPJPY has taken out the bottom end of the declining wedge formation.

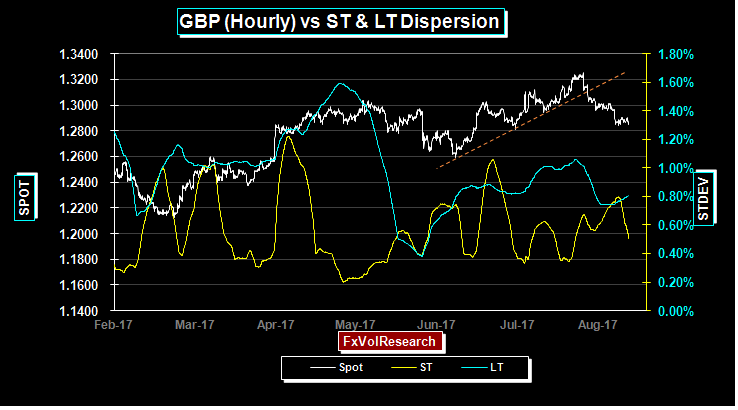

GBP has taken out the hourly trend line.

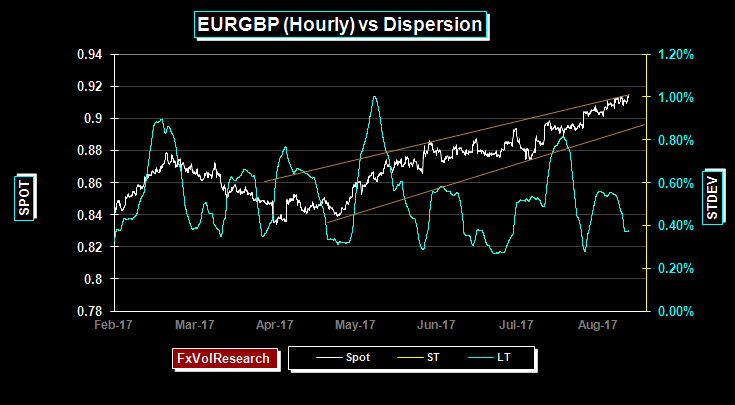

EURGBP holds its upside channel but the odds of a correction back to the bottom end are high.

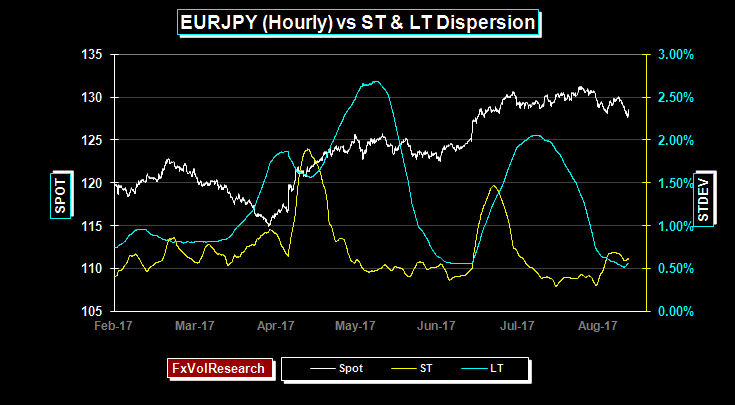

Based on the above the odds of a EURJPY trend is developing in the near term is high. EURJPY has also taken out the hourly trend line (not shown). The odds of a leg lower in EURJPY is high.

Source – James Rider: http://bit.ly/2wvF384