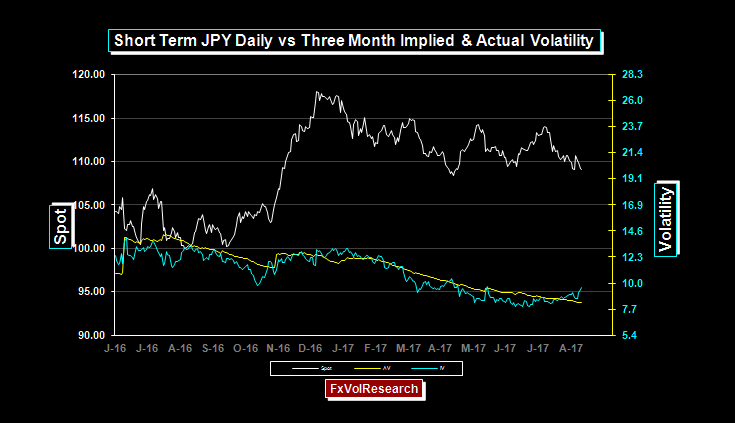

Three-month yen vols are finally rising on the break in the support at the bottom end of the triangle. The appreciation of the yen was characterized last week as a knee-jerk reaction to the Korean crisis. However, the move in the yen is more likely a derivative of the rally in US bonds following the weaker than expected inflation report. If the FX market really was of the view that a hot war was imminent the Yen would not be a likely candidate for appreciation, nor would the KRW or many of the Asian main currency pairs. Having said that the rise in Yen vol is the first sign that the Yen is likely to break out its sideways consolidation pattern. The more likely trigger for a sustained appreciation of the Yen would be a renewed outbreak of risk aversion. Continued volatility and political uncertainty generated by the current US administration would be the most probable cause. Yen risk reversals both vs. the dollar and the major crosses moved smartly better bid for out of the money Yen calls, however as you easily see from the chart above, the premiums for at-the-money options remain historically cheap.

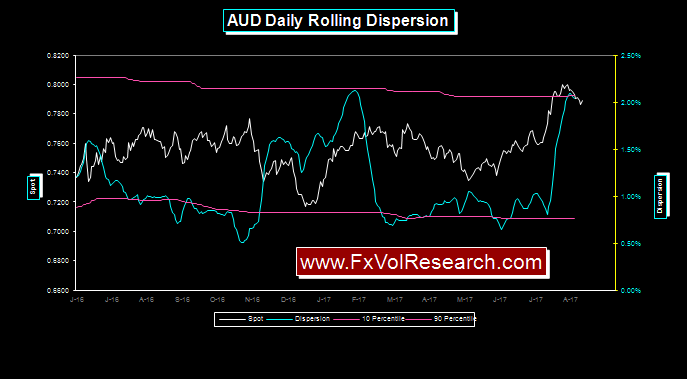

AUD dispersion has rolled over and that implies a period of sideways consolidation going forward with a higher probability of a weaker trend developing. Having said that however it is hard to see the Dollar bloc really selling off unless we see a credible break down in the commodity complex.

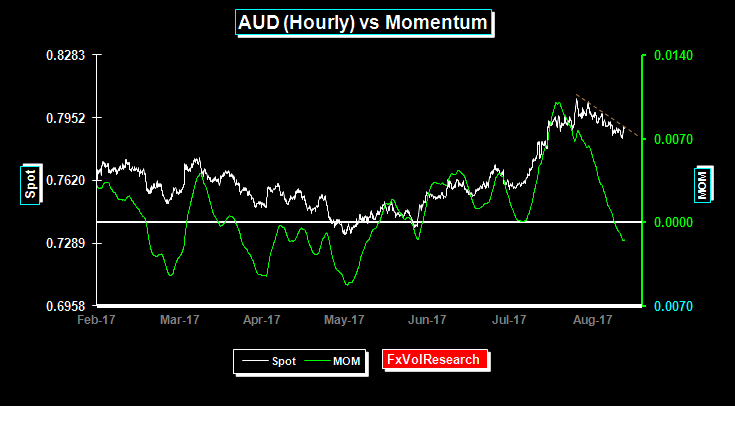

AUM momentum moves into negative territory but it is still to early to call for a major secular turn in the currency.

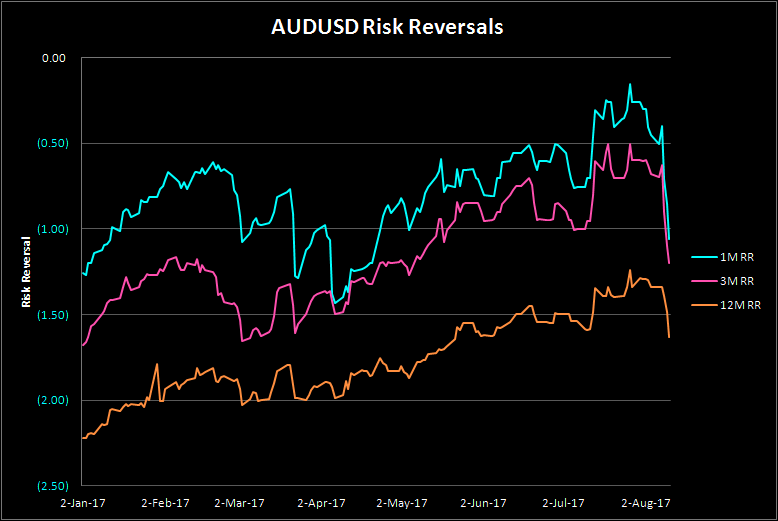

Very strong demand for AUD puts over calls accelerates with only a minor break down in the spot.

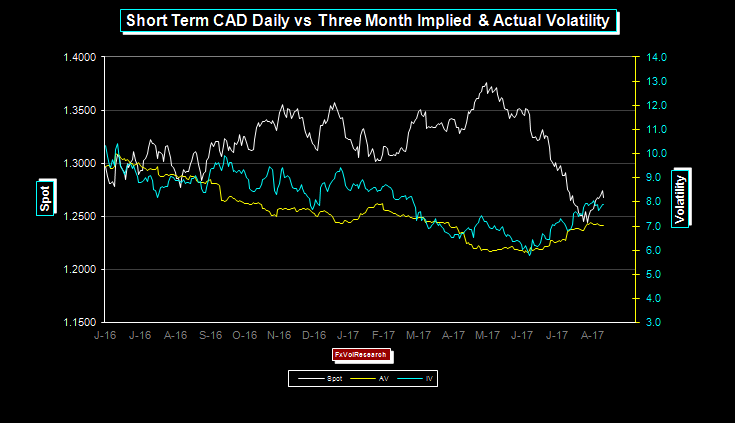

Three month CAD implied vols rise and the spread betweein implied and actuals widens.

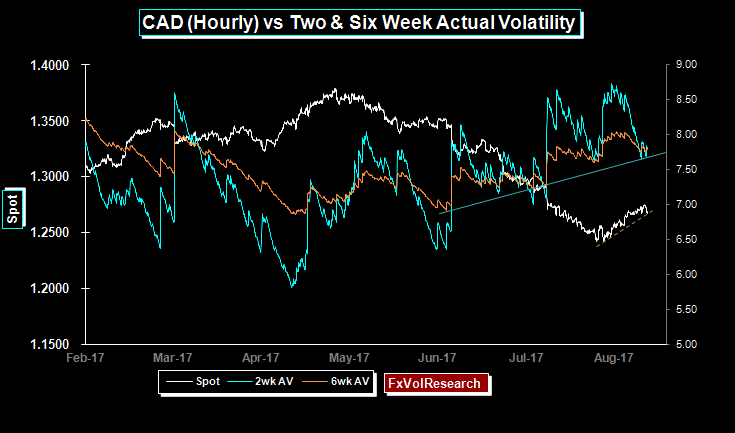

Short term CAD actuals are topping, but have not yet broken down decisively. When they do it will confirm that the CAD is back into a consolidation pattern. CAD risk reversal ended the week largely unchanged with the premiums holding stable for CAD puts over calls.

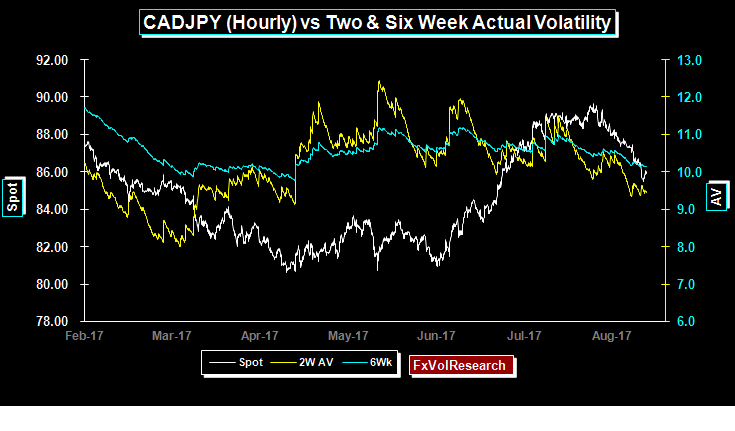

As we pointed out last week with early signs of momentum divergence CADYEN is correcting lower but with declining volatility. Yen strength was a consistent theme across all of the major crosses last week.

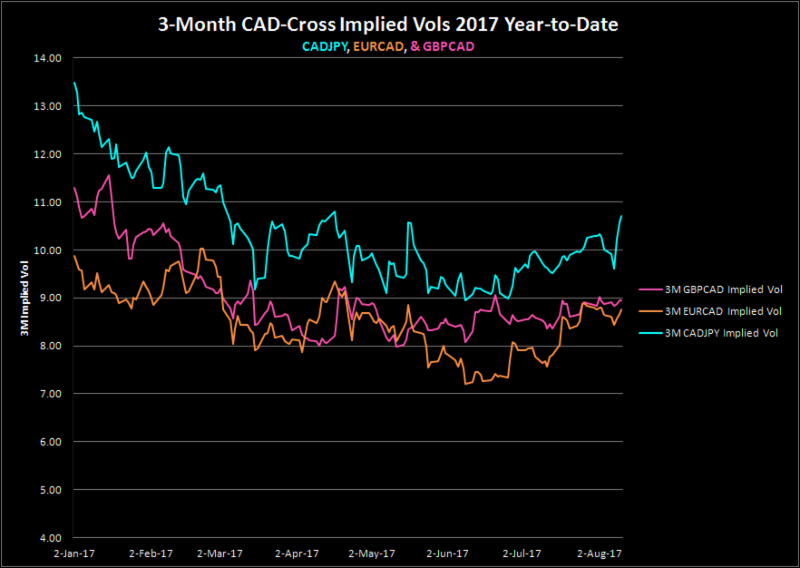

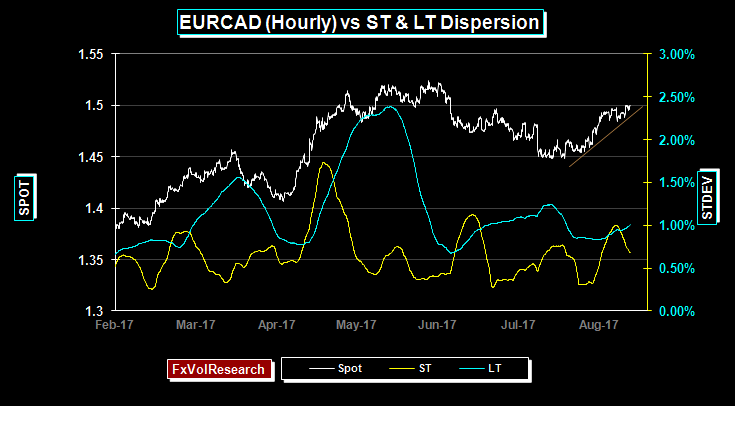

CADYEN follows USDJPY vols higher on the week while GBPCAD and EURCAD remain more subdued by comparison with the latter holding just under the 9% level.

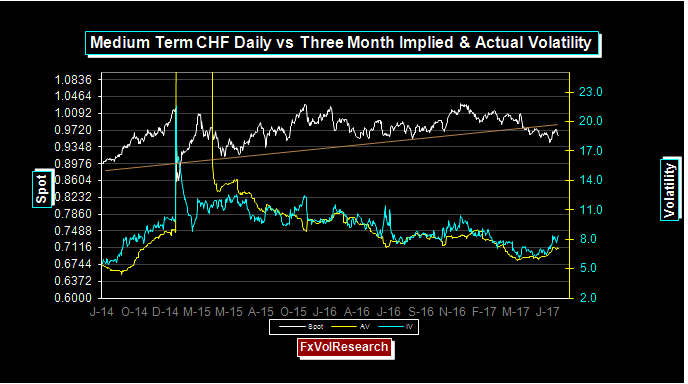

The CHF is still holding below the trend line (see above) despite the short lived $ rally. CHF vols still trending higher and the spread with the actuals is widening. It may not be dramatic but slowly volatility in the major currency pairs is rising.

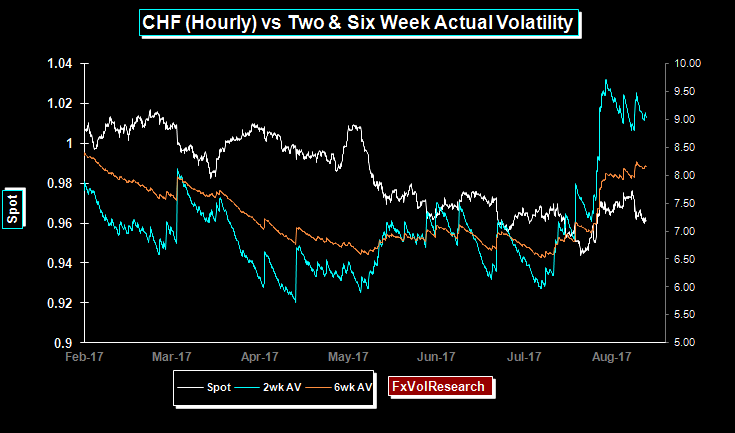

Short term CHF actuals remains at their highs for the year and short dated CHF options are no longer cheap.

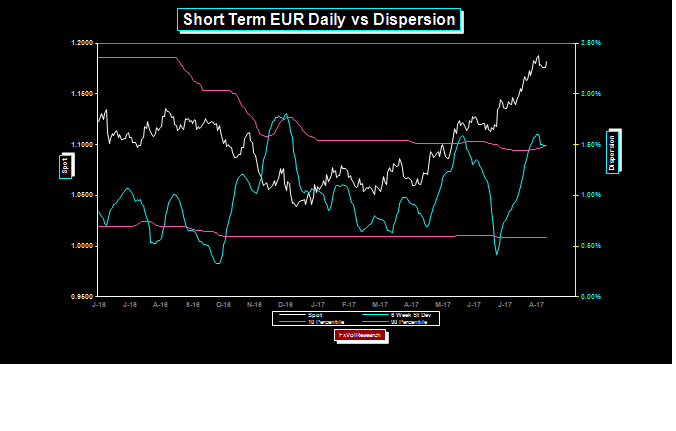

Signs of a top? EUR risk reversals also ended the week flat which implies that most of the street has covered their inventory of out-of-the-money EUR calls. The roll over in the dispersion indicator is often an early sign of consolidation to follow with a higher probability of a larger correction developing. The EUR may need a larger correction back to 1.15 before making a more determined assault on the 1.20 level.

Signs of a top? EUR risk reversals also ended the week flat which implies that most of the street has covered their inventory of out-of-the-money EUR calls. The roll over in the dispersion indicator is often an early sign of consolidation to follow with a higher probability of a larger correction developing. The EUR may need a larger correction back to 1.15 before making a more determined assault on the 1.20 level.